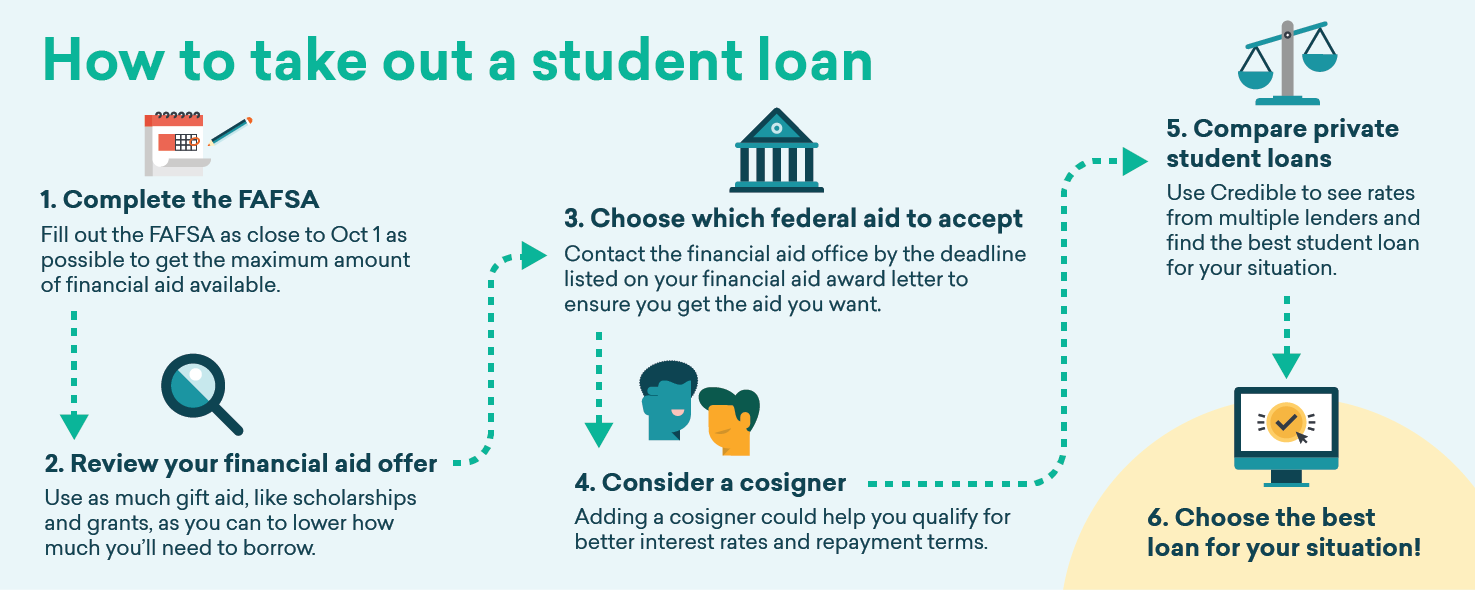

When embarking on the journey of higher education, many students find themselves in need of financial assistance to cover tuition and associated costs. This is often achieved through student loans, which, while providing necessary funds, also come with specific obligations. One of the most critical components of taking out student loans is understanding the legal and financial commitments involved. Among these commitments, the signed agreement that borrowers enter into is pivotal. It is essential for students to grasp the implications of this agreement, as it dictates the terms under which they will repay the borrowed funds.

As students navigate their educational paths, the prospect of repaying student loans can seem daunting. However, understanding what constitutes the signed agreement can alleviate some of that anxiety. This document not only outlines the borrower's responsibility but also serves as a legal framework that protects both the lender and the borrower. It is imperative to be informed about the components of this agreement, including interest rates, repayment schedules, and potential penalties for late payments.

In this article, we will delve deeper into the intricacies of student loans, focusing specifically on the signed agreement known as the promissory note. By examining various aspects of this document, we aim to equip students with the knowledge they need to make informed financial decisions as they pursue their educational goals.

What is the Signed Agreement for Student Loans?

The signed agreement that students enter into when taking out student loans is commonly referred to as a promissory note. This legal document represents the borrower's promise to repay the loan under the specified terms and conditions. The promissory note includes crucial details such as:

- The total loan amount

- The interest rate applicable to the loan

- The repayment schedule and duration

- Any applicable fees

- Information regarding deferment and forbearance options

Why is the Promissory Note Important?

The promissory note serves several important functions. Firstly, it formalizes the loan agreement, ensuring that both parties—the borrower and the lender—are clear about the terms of repayment. Secondly, it provides a legal framework for enforcing the repayment of the loan, should the borrower default. Understanding the significance of this document can help students recognize their obligations and make responsible financial choices.

What Happens if You Default on a Student Loan?

Defaulting on a student loan can have severe consequences. The implications can affect various aspects of a borrower's life, including:

- Negative impact on credit score

- Ineligibility for future federal financial aid

- Wage garnishment

- Tax refund seizure

How to Read and Understand Your Promissory Note?

Reading a promissory note can be overwhelming, but breaking it down into manageable sections can make the process easier. Here are some key components to focus on:

- Loan Amount: This is the total amount you are borrowing.

- Interest Rate: Pay attention to whether it is fixed or variable.

- Repayment Terms: Understand when payments begin and how long you have to repay.

- Default Terms: Know what constitutes default and the consequences.

Are There Different Types of Student Loans?

Yes, there are various types of student loans, each with its own terms and conditions. The primary categories include:

- Federal Student Loans: These loans are funded by the government and typically offer lower interest rates and more flexible repayment options.

- Private Student Loans: These loans are offered by private lenders and may have stricter repayment terms and higher interest rates.

- Subsidized vs. Unsubsidized: Subsidized loans do not accrue interest while the borrower is in school, whereas unsubsidized loans do.

How Can You Avoid Defaulting on Your Student Loans?

To prevent default, borrowers should consider the following strategies:

- Stay informed about your repayment schedule and due dates.

- Communicate with your lender if you encounter financial difficulties.

- Explore deferment or forbearance options if needed.

- Consider enrolling in an income-driven repayment plan.

What Should You Do Before Signing the Promissory Note?

Before signing the promissory note, students should take the time to review the document thoroughly. Here are some tips:

- Ask questions about any terms or conditions you do not understand.

- Compare different loan options to ensure you are making the best choice.

- Consider consulting a financial advisor for personalized advice.

Conclusion: Understanding Your Commitment

When taking out student loans, what do you call the signed agreement to pay? The answer lies in the promissory note, a vital document that outlines the borrower's obligations. By understanding this agreement and the implications of student loans, borrowers can make informed decisions that will impact their financial future. With careful planning and awareness, students can navigate the complexities of student loans and work towards achieving their educational goals without falling into debt traps.